The Hidden Tax at the Pump

Gas just hit $4.11 a gallon — and the pain doesn't stop at the pump. Here's what's really going on, and three budget moves to make this week before it eats into your wealth-building progress.

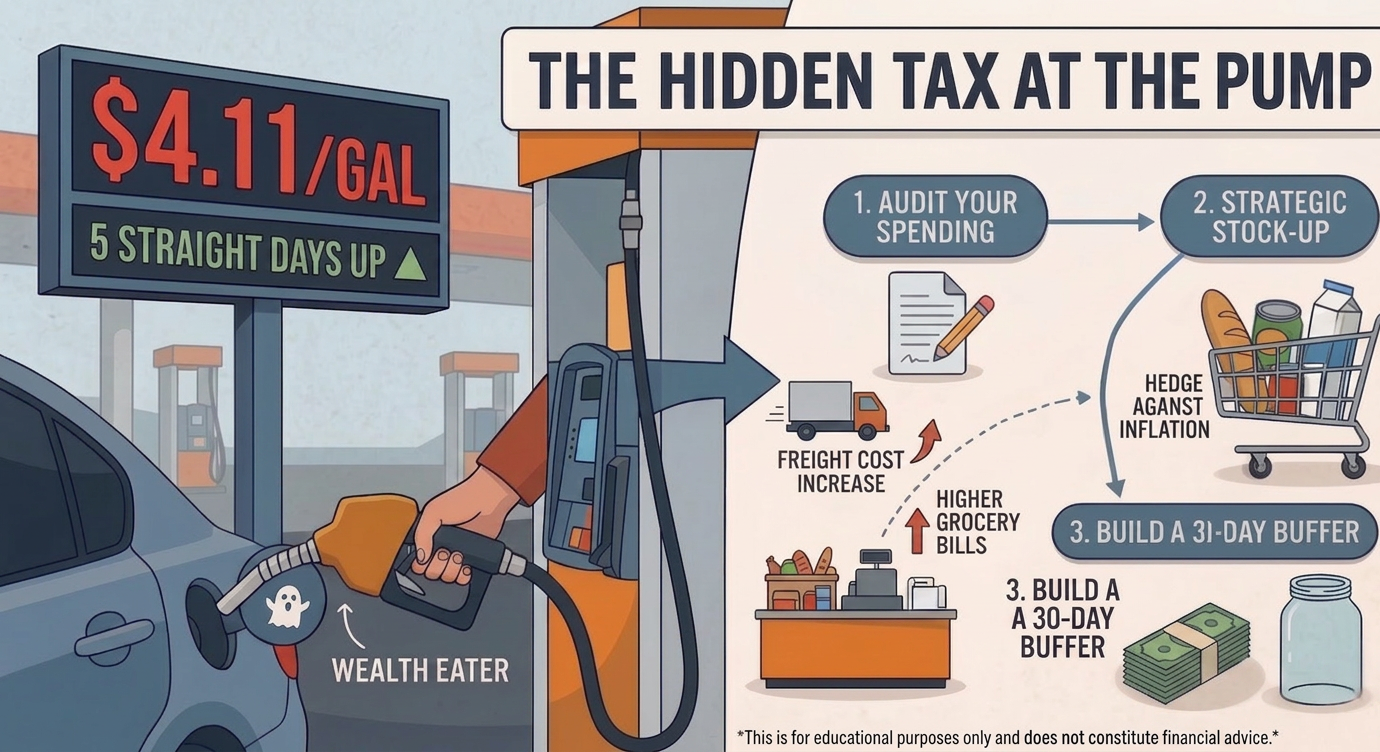

Gas just hit $4.11 a gallon nationally — and it's been climbing for five straight days.

That number alone is enough to make your stomach drop at the pump. But if you think the pain stops there, think again. What's happening at the gas station right now is about to show up in your grocery bill, your delivery fees, and your overall monthly expenses — and most people won't see it coming until it's already hit.

Let's break down what's really going on, and more importantly, what you can do about it before it eats into your wealth-building progress.

What's Driving the Spike

The short answer: geopolitics.

The U.S.-Iran conflict has pushed Brent crude oil past $108 a barrel — nearly 50% higher than before the war started. When crude goes up, everything downstream follows. Gasoline. Diesel. Shipping. Food.

Diesel is already sitting at $5.45 a gallon. That matters more than most people realize, because diesel isn't just for big rigs — it's the fuel that moves everything you buy. Groceries, furniture, Amazon packages, restaurant supplies. When diesel costs more, businesses pay more to move their goods, and they pass that cost straight to you.

The delay? Usually a few weeks. Which means the price pressure you're about to feel in the checkout line hasn't even fully arrived yet.

The Ripple Effect You Need to Prepare For

Here's the chain reaction playing out right now:

Crude oil rises → Gas prices spike → Diesel follows → Freight costs increase → Grocery & retail prices climb → Your purchasing power drops

This isn't a theory. It's a pattern that repeats every time energy prices surge. And with gas up 7 cents in just one week, the momentum is clearly there.

The households that struggle most during these cycles are the ones operating on a "set it and forget it" budget — the ones who haven't looked at their monthly spending in a while and don't have a cushion to absorb cost increases.

3 Budget Moves to Make This Week

You don't need to panic. But you do need to be intentional. Here's where to start:

- Audit Your Variable Expenses

Gas, groceries, and delivery are all variable — meaning they move with the market. Pull up last month's spending in each of these categories and set a new ceiling for the next 60 days. You want to know your baseline before prices push it higher without you noticing. - Stock Up Strategically (Not Emotionally)

This isn't about panic-buying. It's about buying non-perishable staples at today's prices before they reflect the new freight costs. Think proteins, canned goods, and household essentials you'll use anyway. Buying ahead on things you know you'll need is a quiet hedge against inflation. - Build a 30-Day Buffer in Your Emergency Fund

If your emergency fund is thin, a sustained energy spike can chip away at it fast. Even adding $200–$300 to a high-yield savings account right now creates breathing room. The goal isn't perfection — it's not being caught flat-footed.

The Bigger Picture

Rising gas prices are a reminder that your financial plan needs to be built for real-world conditions — not just ideal ones. Markets shift. Global events happen. Costs move without asking permission.

The wealth builders who come out ahead aren't the ones who had the most money when things were easy. They're the ones who stayed proactive when things got bumpy.

You're reading this on a Wednesday. That's already a good sign.

A Next Step

Moments like this are exactly why having a financial strategy built for volatility matters. If you want to assess how well your current plan holds up when costs rise and markets shift — and where tax-advantaged growth could strengthen your position — let's talk.

Schedule your session at www.speakwithjon.com

This post is for educational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making investment or budgeting decisions.

Important Disclosure

Downside Protection Clarification: References to "downside protection" or "0% floor" mean that your principal will not receive a negative interest rate credit during market downturns. This does not guarantee absolute principal protection against all risks, including insurance company insolvency or policy lapses.

Tax-Advantaged Accounts: Tax treatment depends on individual circumstances and may change. Consult with a qualified tax professional regarding your specific situation.

General Information: This content is for educational purposes only and does not constitute financial, legal, or tax advice. Individual results may vary based on personal circumstances.

Jon D. O'Neil is a licensed financial professional. For personalized guidance, schedule a consultation at www.speakwithjon.com

Found this helpful? Share it:

Jon D. O'Neil

Jon D. O'Neil is a wealth partner with over 10 years of experience helping clients achieve financial wellness through debt elimination, tax-advantaged accounts, and lifetime income strategies. Based in Lewisville, TX, Jon specializes in creating personalized financial solutions that provide stability and growth without market volatility.

Schedule a consultation →